Delinquencies were increasing before the virus outbreak. What happens now? Even before the massive drop in economic activity due to COVID-19, there were signs of trouble brewing on the subprime loan side of the auto lending market. Now more than ever, it's important for subprime lenders to understand and effectively manage these delinquencies.

Subprime Loans by the Numbers

While a subprime borrower has a lower credit score and presents a greater credit risk than an average borrower, the definition of “subprime” in terms of credit score varies. For our purposes, we’ll consider subprime to be a credit score of less than 620.

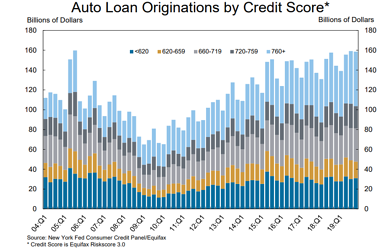

Auto debt is the 3rd largest debt category in the US after mortgages and student loans. It now makes up 10% of total household debt. The Federal Reserve Bank of New York issues a quarterly household debt study and based on its most recent study, and as seen in the chart below, about 15% ($25 – 30 billion) of 2019:Q4 auto loans are considered subprime.

Per financial analyst Wolf Richter, severe delinquencies on subprime auto loans have exploded, surging to a new record as of February 2020. Out of the $1.3 trillion in auto loan and lease balances, we know around $25 billion are subprime. We also know that almost a quarter, approximately $66 billion, were 90+ days delinquent in the fourth quarter of 2019. And this was before the virus outbreak.

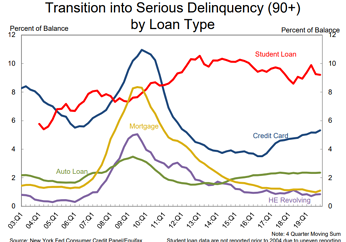

At 90+ days delinquent, we all know the unfortunate reality: these borrowers are unlikely to come back and make the balance current again. Here’s another interesting chart from the Federal Reserve Bank of New York, showing 2.5% of all auto loans are 90+days delinquent, up 0.5% since 2014 and steadily increasing (NY Fed Debt Survey, slide 14).

Cox Automotive, owners of Kelley Blue Book & AutoTrader, reports that severely delinquent accounts are up 5.4% year over year, painting a tough picture for subprime auto lenders.

What Can Subprime Auto Lenders Do Now?

As a subprime auto lender, you are, in part, stuck with the paper you have in your portfolio. Loans have been written and need to be serviced. So what to do now? Here are some simple but effective steps to take:

- Be proactive and maintain contact with the investor groups that buy your loans.

- Expand your payment options to make paying on existing loans as easy as possible for borrowers. Consider online payments, IVR (Interactive Voice Response), and text pay so borrowers can pay via cards and bank accounts whenever they have the cash available.

- Adapt communication styles to your borrowers’ preferences – implement text messaging services to send payment reminders and account updates.

- Ensure all relevant paperwork is complete, so you have what you need if the loan goes south.

- Fine-tune and be ready to show your collection and repossession procedures to prepare for any incoming repossessions.

There’s not much else you can do with your existing loans as they move through the servicing cycle, but you can use this information when evaluating new loans. However, it’s important to keep in mind our upcoming post-COVID-19 world.

The NY Post reports IHS Markit projects 2020 auto sales will drop by 15% compared to 2019. The NY Times reports analysts estimate a drop of about 37% in 2020 Q1 due to March’s shelter in place orders.

There are so many unknowns right now. Will the $1,200 per person stimulus package be the only public stimulus? Will more consumer-friendly legislation follow? Will consumers use that $1,200 to pay down debt? Issues surrounding job and home security abound.

We simply don’t know what will happen on a personal or economic level.

The one piece of ‘good news’ for subprime lenders is that more borrowers will need your services in the future. Banks and credit agencies will continue reporting on consumers’ pay habits, even if borrowers are allowed a debt holiday or a forbearance. As credits degrade in the upcoming months, more will need your services to finance their next cars. If you put some safeguards in place, you may be able to make the most of the situation. These safeguards include:

- Verifying current employment

- Increasing down payments and lowering finance amounts

- Confirming bank balances to ensure personal liquidity

- Exercising caution when underwriting for consumers in the states of New York, New Jersey, California, Arizona, and Nevada, the most debt-heavy states (NY Fed Debt Survey, slide 32)

- Carefully evaluating 18- to 29-year-old consumers, the demographic with the most trouble paying current bills (NY Fed Debt Survey, slide 26)

You know it’s going to be a tough time post-COVID-19, at least in the short term. However, there are concrete steps you can take to prepare your lending business for what’s coming next. How will you adjust?